One of the more eye-opening aspects of the first “So Who’s Using DITA?” article I posted here a year ago was the variety of firms that had adopted DITA in some part of their documentation process. While those results were dominated by the number of software firms using it, what I found most interesting was how many other types of companies and organizations were also using DITA.

When compiling the most recent update to the Companies Using DITA listing, I decided to revamp the “Company Types” categories in the hopes of getting a clearer picture as to the background for each firm. Previously I had been using Wikipedia to help classify the firms, as the WP template for companies always lists the industry type. My problem was that almost 40% of the firms had no page on Wikipedia, leading me to make some educated guesses. Then I found that LinkedIn provided a more comprehensive alternative, with more-or-less consistent industry categories listed for each firm in its database, so I have combined that data with the firms I have listed.

The results are interesting, as I think you will agree…

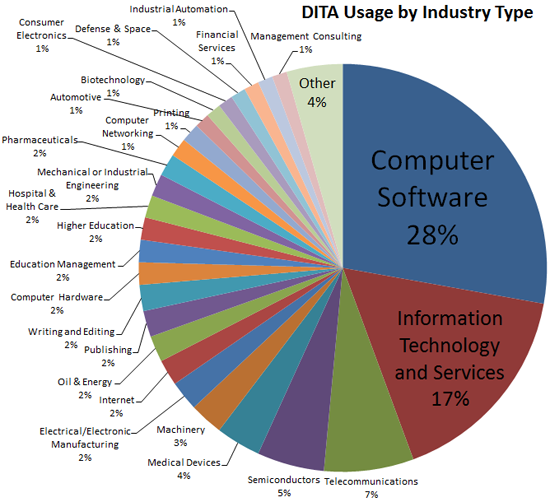

Computer Software

It should come as no surprise that computer software comprises the largest single category, comprising 25% of the total. DITA had its origins in this sector along with many of its initial adopters and from the get-go there were obvious cost/efficiency benefits for using DITA as the basis for tackling things like online help and especially localization. A short list of some of the firms in this category reads like a Who’s Who of the software industry:

- Adobe

- Autodesk

- Borland

- Compuware

- FICO

- Platform Computing

- Jack Henry and Associates

- Minitab

- Progress Software

- Quark

- SAP

- Sybase

- VMware

- Webtrends

This is a selection of the nearly 100 firms comprising this category, all of whom are using DITA in some way in their documentation processes.

Information Technology and Services

The Information Technology and Services industry category is somewhat broad in its definition, comprising everything from consulting firms to computer components, management services, databases and more. It seems to be a catch-all category for companies that are known for having more than a single focus. A short list of some of the firms in this category includes:

- Northern Arizona University

- CEDROM-SNi

- Dell Kace

- EMC

- Hitachi Data Systems

- IBM

- Jorsek

- NetApp

- Oracle

- Ricoh

- Tech-Tav Documentation

- Xerox

As you can see this is a diverse set of companies, and all told there are 56 companies so described in this category.

Telecommunication and Semiconductor Firms

Next come two well-defined categories: telecommunications and semiconductor firms. These comprise both phone manufacturers (Ericsson, Research in Motion, Nokia and Sony Mobile Communications), related equipment and research (Alcatel-Lucent, Hughes Network Systems and Tellabs), related software (Symbian and Sandvine for example), to telecomm networks (Telus for example). Given the number of firms in this sector (25) it is surprising that there is no DITA telecommunications specialization in the works, though admittedly even this category can be considered broad in its scope.

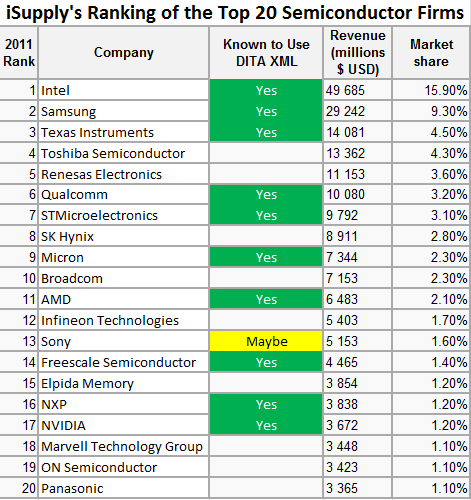

One of the questions I have been asked is how pervasive is DITA usage within a particular sector? The semiconductor industry is a relatively well-defined sector, and as part of a presentation I did last year I compared my list of semiconductor firms against the “Top 20” such firms as defined by the market intelligence firm iSuppli. What I found back then (and is still true today) is that about half of the firms are using DITA in some way. None of the newly-added firms are in this list, though I have several on a watch list of firms that I strongly suspect (but can’t as yet prove) are using DITA, so I suspect the percentage is actually higher.

Medical Device and Machinery Companies

While in many of the other sectors I suspect that I am simply discovering firms that have been using DITA XML for some time, I believe that there is significant growth happening for DITA adoption in these two sectors. I can’t point to any specific fact that leads me to think this, other than it seems like there are significantly more firms in these sectors than I found when I last ran this survey. The first category is comprised of firms producing information technology for the health care sector. For example, Allscripts provides electronic health record technology, Elekta and Varian Medical Systems produce radiation therapy equipment, Horiba makes automated analysis devices,

and Ortho Clinical Diagnostics creates in vitro diagnostics products. Given that this sector is heavily regulated it tells me that the relative success of DITA adoption in this sector proves that it cannot only stand up to rigorous regulatory scrutiny, but due to the myriad of tools and CCMSes available, likely makes this process easier to manage.

Firms in the machinery sector are a mixed bag, including the likes of:

- AGCO

- Caterpillar

- Gleason

- Husky Injection Molding Systems

- John Deere

- Joy Mining Machinery

- Massey Ferguson

There’s a significant portion of agricultural machinery firms in this category, mixed in with those that make mining equipment and machine parts.

The 2% Category of Firms Using DITA

While 2% may not seem like a lot, given the size of the Companies Using DITA list, it means that I have been able to track down at least six firms that fall into this category. The categories themselves are diverse:

- Electrical/Electronic Manufacturing (Samsung, Schneider Electric)

- Internet (Amazon, PayPal)

- Oil and Energy (Chevron, Schlumberger)

- Publishing (XML Press)

- Writing and Editing (iDTP, Paradigm Information Services)

- Computer Hardware (Epson, Nvidia)

- Education Management (Kaplan, Texas A&M Engineering Extension Service (TEEX))

- Higher Education (Brigham Young University, Northern Arizona University)

- Hospital and Health Care (Agfa Healthcare, Siemens Healthcare)

- Mechanical or Industrial Engineering (Carrier Corporation, Johnson Controls)

- Pharmaceuticals (Lorenz Life Sciences, U.S. Pharmacopeial Convention)

As you can see, this is a very diverse set of industries that are using DITA, which speaks to the versatility of this XML specification if nothing else.

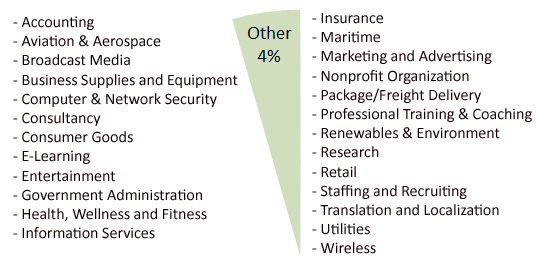

What is “Other”?

There are also a number of firms in the 1% category (including companies in the Automotive, Consumer Electronics, Financial services and Defense), but there are also a significant number of firms I’ve had to place in the “Other” category, sometimes comprised of only single firms that I have found belonging to a particular industry category. The following graphic provides a glimpse as to what that “sliver” from the opening chart is comprised of:

In this as in all of the other company categories, DITA is being used far and wide throughout just about any industry you can think of.

Tomorrow: What are the sizes of the companies that are utilizing DITA? Is company size a factor in DITA adoption rates?

Hi Keith,

Thanks for putting this together, it’s fascinating. We’ve seen the DITA industry really take off in Hi Tech and Software and now start to mature, which is obviously reflected in your study. A lot of our customers helped fuel the expansion of that industry. The growth areas that we are starting to see now are in areas like Medical Devices and Life Sciences, so it’s good to see that your study validates that. Interestingly, considering it’s only at 1% right now, we are also seeing growth in Financial Services and Insurance, where companies are looking to tackle compliance, consistency of terms and conditions, and treating credit cards and insurance packages as ‘products’, for instance.

Interested to see the next post and also a comparison of results over time next year. Thanks for this!

Tom

SDL

Thanks Tom (also for the re-tweet)! I also found it interesting to see that DITA is clearly expanding in sectors other than in software, where it all started. It is also interesting to here more about the “why”, as in, what the particular benefits are for firms adopting DITA in those sectors.

If you have any customers in those sectors that you mention who would be willing to talk to me about what the specific benefits of DITA are to them for a future piece on DITAWriter.com, I would definitely be interested.

Hi Keith,

Thank you for sharing the results of your survey.

It looks very interesting and confirms our own observations. In 2012, we, at DITAToo, have got several customers and leads from industries other than software and IT (mechanical engineering and financial services).

Their key business drivers were mostly the same as the reasons that software companies usually give: the need to effectively reuse content, reduce translation costs (it’s especially critical for European customers), and enforce consistency and compliance. The last one was a focus of the financial services company we are working with.

One of differences between software/IT companies and customers coming from other industries (especially financials) we noticed is the need to have a more user-friendly authoring environment that doesn’t require deep knowledge of DITA. While technical writers usually don’t have a problem to author in a DITA editor, a financial consultant obviously wants to stay in Word or Word-like environment.

This brings us to the question about the future of DITA editors, the growing need for lightweight DITA editors, and potential of DITA to become an enterprise-wide standard. I think a success of DITA in industries beyond software and IT to a great extent will depend on whether DITA tools (authoring, publishing, and managing) will become more user-friendly and understandable for non-technical writers.

Alex

DITAToo

Hi Keith, this is very interesting data. Another way to look at this might also be to look at the size of companies using DITA, and also the volume of information.

In general, I think most people assume that structured writing is most adapted to organisations with huge amounts of information to manage, via a CMS. Yet I am currently doing a project with a small startup, for one software product, with a relatively small amount of information. For now, we’re using their software configuration management repository instead of a CMS, though a CMS will probably be needed in the future.

Why use DITA for such a situation? Because this software gets highly customized at each installation – there is need for several layers of embedded user assistance:

Generic information

Industry-specific information

Installation-specific information

The only reasonable way to do this is using lots of variables, conditional text, and a high level of automation, which we are only beginning to develop.

DITA provides the simplest path to getting those things, though it is not simple at all.

As for the “size of the companies using DITA” question, you’ll find an answer to that in today’s post on the site. I was also surprised by the results as I had thought it would lean heavily towards larger companies, but it really does seem like with DITA “one size fits all”. Its not quite as simple as that, but the standard is clearly scalable.

I can’t answer the “volume of information” though, not definitively at any rate. I’ve not been able to track down any definitive marker that marks out DITA-produced content as opposed to some other process that would allow me to give an estimate. It’s safe to say it is growing, but it is hard to say exactly by how much.

I agree with you that DITA provides the simplest path to getting those things, though I disagree with your final clause, and just say that it is as simple (or complicated) as it needs to be. This is where a good Document/Information Architect can make a real difference, guiding the writing staff, restricting the number of tags implement to what is actually useful, devising a reuse model that is optimized for the needs of the writers, etc. Don’t confuse depth with complexity. 😉

“Don’t confuse depth with complexity” – you betcha!

However, complexity does exist. It is not bad in itself, we just need strategies for managing it – and that’s what I was writing about in my reply – as I think you also agree.

The principle that we should keep things simple does not mean to over-simplify or schematize – just that things are complex enough, without making them more so, right? 😉

Exactly right! Couldn’t agree with you more.

I’m curious about your Semiconductor industry chart – From my experience most of the user-facing documentation that this industry creates is in the form of data sheets, reference designs, and API-type publications. At the same time, DITA is marketed to as primarily enabling goal-oriented documentation. I’m not sure if this is a messaging issue or what, but semiconductor industry documentation generally seems to be far from a goal-oriented design. Why is their adoption rate so high?

I’m not Keith, but I probably have an answer to this question. My guess is it’s happening because:

1. The amount of reusable content in semiconductors industry is high: the same data is used in multiple datasheets plus in some datasheets the data have to be customized per product.

2. Consistency in structure (and formatting) is critical: all the reference tables, API commands, etc. should look the same across multiple documentation sets.

But I’d be happy to hear what content authors from semiconductors industry would say!

Yes, nice summary of my points below (which answers the original comment).

I think there is more than one reason for this, but a key one is definitely the ability to re-use content. You are right that the majority of docs produced for the semiconductor sector are not typical end-user, goal-driven docs (though there are always exceptions to this rule) but there are many instances where things like registry settings are used again and again and again (and again and again), so there’s a strong argument there not only for reuse but for consistency. Many of these firms also localize their content, so the savings that can be had from reusing content that has already been translated is considerable.

Another reason which I suspect has made its way through the mindset in this industry (and likely other sectors as well) is that retaining such content — especially if it is in a searchable CMS — is a way of instating a form of corporate memory. For example there is often a considerable amount of time between when an engineer designs a component and when it ships, at which point they are then, belatedly asked to document what they did. Not surprisingly, this can cause problems… 😉 If engineers are asked to capture their design information early in the process in a centralized CMS it makes it much easier to troubleshoot a product containing that component when it ships. Am not saying that all semiconductor firms are thinking this far ahead, but this is a realization that has hit a couple of firms that I am aware of.

The benefits are enough for this sector that there is an active semiconductor specialization in the works, which may go out with DITA 1.3.

Hope that answers your question!